TAX AUDIT STRATEGY FROM 01 JULY 2026: THE ERA OF “RISK-BASED MANAGEMENT”

Under the impact of the new Law on Tax Administration, the tax authority will fully transition from a periodic / broad-based audit model to a data-driven, risk-based audit approach.

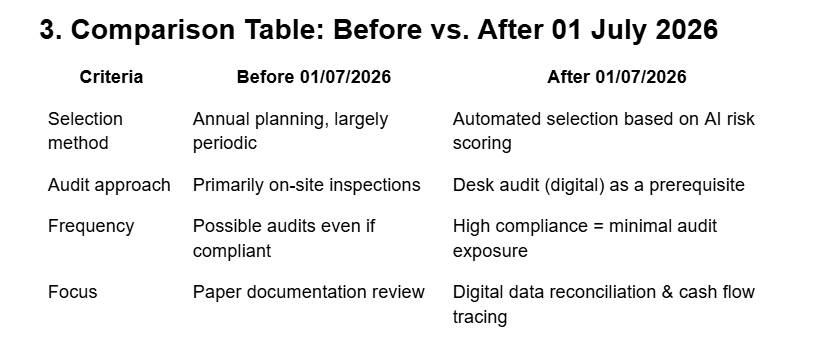

New Operating Philosophy: “Digital First – On-site Later”

Before issuing any on-site inspection decision at an enterprise (the “Enterprise”), the tax authority will conduct a desk audit using advanced systems (AI & Big Data):

Data cross-matching: Reconciliation of e-invoices – tax returns – financial statements – bank statements.

Risk scoring: Automatic classification of each tax identification number into risk tiers (Green – Yellow – Red).

Pre-audit clarification filtering: Only where the Enterprise fails to sufficiently explain detected anomalies will an on-site inspection be triggered.

Six “High-Risk (Red Flag)” Target Groups Subject to Audit

🟢 Group 1: Tax Refunds (Top Priority)

Pre-refund audit: Applicable to first-time refund claims or cases with unusual input suppliers.

Post-refund audit: Applicable to Enterprises granted refunds under priority treatment but subsequently flagged for risks (e.g., fictitious invoices).

🔵 Group 2: Structural and Legal Changes

Events that alter the tax identity of an Enterprise, often associated with risk of historical non-compliance concealment:

Demerger, merger, consolidation, equitization;

Dissolution, bankruptcy, tax code deactivation;

Notably: Relocation across jurisdictions (to prevent “regulatory evasion” between localities).

🔴 Group 3: Data-driven Risk Indicators (AI Detection)

AI-based analytics will flag anomalies such as:

Industry inconsistencies: Significant revenue growth with disproportionately low tax payable, or margins materially below industry benchmarks;

Invoice ecosystem risks: Transactions with blacklisted entities or suppliers abandoning registered business addresses;

Related-party transactions: Indicators of transfer pricing, including excessive interest expense allocation.

🟡 Group 4: Tax Incentives and Exemptions

Enterprises claiming tax exemptions, reductions, or non-taxable status but failing to meet qualifying financial or operational criteria

(e.g., high-tech enterprises without corresponding R&D expenditure).

🟣 Group 5: Thematic Audits (Sector-focused Campaigns)

Targeting high-risk sectors with significant revenue leakage potential:

E-commerce: Livestream sales, individual sellers on digital platforms;

Real estate: Under-declaration of transfer values;

FDI enterprises: Persistent losses alongside business expansion (profit shifting concerns).

🟠 Group 6: Whistleblowing and Complaints

On-site verification based on denunciations from individuals, employees, or intelligence from other authorities

(e.g., Police, State Bank).

Practical Conclusion: What Enterprises Must Do

From 2026 onward, “data integrity” outweighs “document presentation.”

Internal audit: Engage advisors to conduct monthly input invoice reviews, rather than waiting for year-end finalization;

Cost rationalization: Ensure all expenses demonstrate commercial substance and logical linkage to revenue

(AI will detect inconsistencies such as fuel expenses without vehicles or excessive labor costs without social insurance contributions);Audit defense readiness: Maintain pre-prepared explanation dossiers for significant financial fluctuations to resolve issues at the desk audit stage.